You probably already have money invested. A 401(k) through work, maybe an IRA you opened years ago. There's a number somewhere — you've seen it on a statement — but if someone asked you how your portfolio is actually set up, you'd have to look it up.

That's not a character flaw. It's just how these things go. You've been busy.

But here's what that means practically: a decision has already been made on your behalf, either by you years ago or by a default enrollment setting. And that decision — how your money is divided between stocks, bonds, and cash — turns out to be the single most important factor in determining your long-term returns.

Not which funds you picked. Not which companies are in them. The ratio. That's what the research says, and the stakes are real enough that it's worth understanding why.

What asset classes actually are

Before we get to the research, you need to understand what these three buckets are.

Stocks are ownership stakes in businesses. When you buy a share of a company, you own a small piece of it — its profits, its growth, and its losses. Over long periods, stocks have historically delivered the highest returns of any asset class. They also crash the hardest when things go wrong. That volatility is the price of the higher return.

Bonds are loans. When you buy a bond, you're lending money to a government or a company in exchange for regular interest payments and your principal back at the end. Bonds are more stable than stocks — they don't swing as wildly — but they also grow more slowly. They're the ballast in a portfolio, not the engine.

Cash means money sitting still — savings accounts, money market funds, certificates of deposit. Cash doesn't grow meaningfully over time, especially after inflation. It has its place, but as an investing strategy on its own, it loses the long game.

That's it. Three buckets. Every portfolio in the world is some mix of these three.

The research that changed how advisors think

In 1986, a team of researchers — Gary Brinson, L. Randolph Hood, and Gilbert Beebower — set out to answer a simple question: what actually determines how a portfolio performs?

They studied 91 large pension funds over a 10-year period. These were sophisticated institutions with professional managers actively picking securities, timing the market, trying to add value every way they knew how.

The finding: 91.5% of the variability in returns was explained by asset allocation policy — not which specific securities the funds held, and not when managers chose to buy or sell.

Let that land for a second. Of all the things these professional investors were doing — the stock picking, the market timing, the tactical moves — none of it explained performance as well as the simple question of how much they had in stocks, how much in bonds, and how much in cash.

This isn't an obscure finding. It's been replicated and expanded over decades. The core conclusion has held: the ratio is the decision. The rest is noise around the edges.

For you as an individual investor, this means something practical. You can spend years trying to pick the right funds within your stock allocation. But if your overall allocation is wrong — if you're taking more risk than you can handle, or not enough to reach your goals — those stock picks won't save you.

What this actually means for your portfolio

Here's a concrete way to see why this matters.

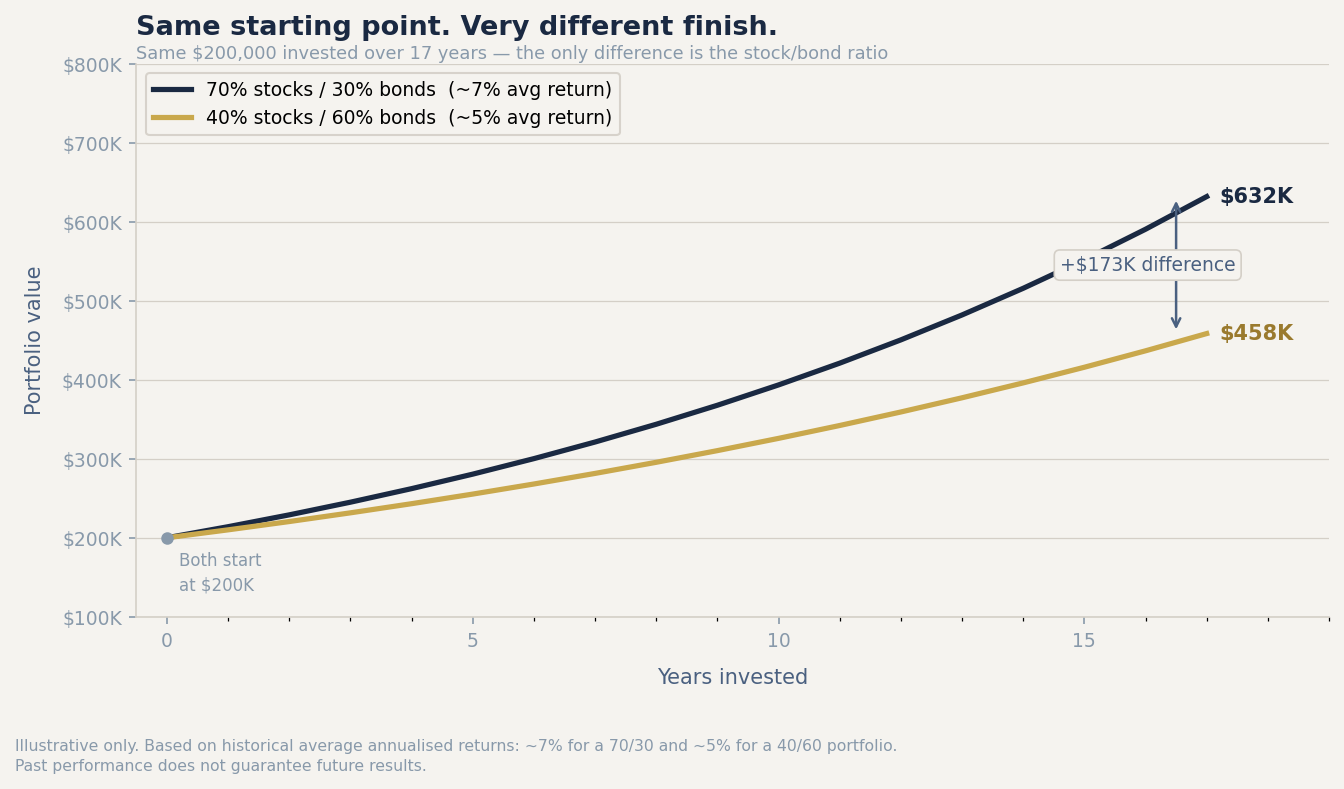

Say you're 48, you have $200,000 in your 401(k), and you're planning to retire around 65. Log in and check your current allocation. You might find you're at 70% stocks and 30% bonds — or you might find you're at 40% stocks and 60% bonds. Both are common. Both feel like reasonable defaults.

But they're not equivalent. Using historical average returns, the 70/30 portfolio grows at roughly 7% annually; the 40/60 portfolio grows at roughly 5%. Applied to $200,000 over 17 years, that gap compounds into a difference of more than $170,000 at retirement — not because of which funds you picked, but because of that ratio.

The 70/30 portfolio will swing harder. In a bad year, you might watch your balance drop 25–35%. But it also captures more of the long-term growth that stocks provide, and over 17 years that compounds into significantly more at retirement. The 40/60 portfolio will feel more stable — smaller drops, less anxiety — but you're trading away growth in exchange for that calm.

Neither is wrong in the abstract. But one of them is wrong for your situation, depending on your timeline, your other income sources, and how you actually behave when markets fall.

There's one more reason this question is more urgent at 48 than it would have been at 28 — and it's something most people don't know about until it's too late.

It's called sequence-of-returns risk. The idea is this: a market crash early in your career is actually fine. Your balance is smaller, you're still contributing, and you're buying more shares at lower prices. A crash right before or at the start of retirement is a different story. Your balance is at its peak, you're about to start drawing it down, and selling into a falling market locks in losses you may never recover from.

This is why an allocation that felt aggressive at 35 — heavy in stocks, riding the swings — may need to look different at 52. Not because stocks are bad, but because the consequences of bad timing are much higher when you're 13 years from needing the money.

The point: this decision is already made. The question is whether it was made intentionally — or just because you never changed the default.

A simple starting framework

The classic starting point is the "age in bonds" rule of thumb: whatever your age, put that percentage in bonds. The rest goes in stocks.

Under this heuristic, a 48-year-old holds 48% bonds and 52% stocks. A 55-year-old holds 55% bonds and 45% stocks. As you age, you shift from growth-seeking to stability-seeking — which makes sense, because someone with 15+ years until retirement can ride out a bad crash, while someone five years out can't afford to wait for a recovery.

Is this rule perfect? No. It's a starting point, not gospel. Your risk tolerance, income stability, and goals all matter. Some investors are genuinely fine with more volatility and should hold even more in stocks. Some are not, and shouldn't.

But here's the value of the rule: it gives you a principled basis for your first decision. You're not guessing. You're applying a logical framework and then adjusting from there.

If you don't want to think about this at all, target-date funds do it automatically. A target-date 2040 fund, for instance, is built for someone planning to retire around 2040. It starts heavily weighted toward stocks and gradually shifts toward bonds as the date approaches. One fund, hands-off allocation management, no ongoing decisions required. It's not exciting. It works.

One action this week:

Log in to your 401(k) or IRA and find your current allocation. Write it down: X% stocks, Y% bonds. Then check it against the age-in-bonds rule. Is it close? Way off? Either answer is useful — you now know something you didn't know before.

That's the foundation. Everything else builds on it.

Next Wednesday: Once you have your allocation, here's the simplest way to actually build it — and why most people overcomplicate what should be a two-fund portfolio.